Joining an Early Stage Startup? Negotiate Your Startup Equity and Salary with Stock Option Counsel Tips

Startup equity negotiation tips for early stage founders, executives, employees, consultants and advisors.

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Startup Equity @ Early Stage Startups

"Hey baby, what's your employee number?" A low employee number at a famous startup is a sign of great riches. But you can't start today and be Employee #1 at OpenAI, Discord, or one of the other most valuable startups on Earth. Instead you'll have to join an early-stage startup, negotiate a great equity package and hope for the company’s success. This post walks through the negotiation issues in joining a pre-Series A / seed-funded / very-early-stage startup.

Q: Isn't startup equity a sure thing? They have funding!

No. Raising small amounts from seed stage investors or friends and family is not the same sign of success and value as a multi-million dollar Series A funding by venture capitalists.

Carta’s data team published an update in December of 2023 showing the “graduation rates” from Series Seed to Series A within 2 years. They affirm that it’s not a sure thing to graduate from Series Seed to Series A and, therefore, even have the chance to make it all the way to a successful acquisition or IPO. In hot years of 2021-2022, the graduation rate hovered around 30% across all industries. In 2023, it ranged from:

23% for FinTech

20% for HealthTech

19% for Consumer

17% for SaaS

16% for Biotech

Here's an illustration from Dustin Moskovitz's presentation, Why to Start a Startup from Y Combinator's Startup School on the chances so "making it" for a startup that has already raised seed funding. These 2nd Round “graduation” numbers are higher than Carta’s numbers, as this data was from 2017 (a hot hot time for startup funding).

What are the chances of a seed-funded startup becoming a "unicorn" (here, defined as having 6 rounds of funding rather than the classic “unicorn” definition of a $1 billion valuation).

Q: How do you negotiate equity for a startup? How many shares of startup equity should I get?

Don't think in terms of number of shares or the valuation of shares when you join an early-stage startup. Think of yourself as a late-stage founder and negotiate for a specific percentage ownership in the company. You should base this percentage on your anticipated contribution to the company's growth in value.

Early-stage companies expect to dramatically increase in value between founding and Series A. For example, a common pre-money valuation at a VC financing is $8 million. And no company can become an $8 million company without a great team.

Imagine, for instance, that the company tries to sell you on the offer by insisting that they will someday be worth $1B and, therefore, your equity worth, say, $1M. The obvious question would be: Does it feel fair to you to make a significant contribution to the creation of $1B in value in exchange for $1M? For most people, the answer would be “no.”

Or, consider that the company is insisting that an offer of 1% is “worth” $1M because the company expects to raise a Series A - based in part on your efforts - at a $100M pre-money valuation. Leaving aside the wisdom (or lack thereof) of evaluating the offer based on its future value, you would want to ask yourself: Does it feel fair to you to make a significant contribution to the creation of $100M in value in exchange for $1M in equity (which would presumably be only partially vested as of the Series A)?

That would depend, of course, on how significant your contribution would be. And it would depend on the salary component of the offer. If the cash compensation is already close to market level, that might seem more than fair. If the cash offer is a fraction of your opportunity cost, you would be investing that opportunity cost to earn the equity. The potential upside would need to be great enough to balance the risk of that investment.

Q: Is 1% equity in a startup good?

The classic 1% for the first employee may make sense for a key employee joining after a Series A financing, but do not make the mistake of thinking that an early-stage employee is the same as a post-Series A employee.

First, your ownership percentage will be significantly diluted at the Series A financing. When the Series A VC buys approximately 20% of the company, you will own approximately 20% less of the company.

Second, there is a huge risk that the company will never raise a VC financing or survive past the seed stage. According to CB Insights, about 39.4% of companies with legitimate seed funding go on to raise follow-on financing. And the number is far lower for seed deals in which big name VCs are not participating.

Don't be fooled by promises that the company is "raising money" or "about to close a financing." Founders are notoriously delusional about these matters. If they haven't closed the deal and put millions of dollars in the bank, the risk is high that the company will run out of money and no longer be able to pay you a salary. Since your risk is higher than a post-Series A employee, your equity percentage should be higher as well.

Q: What is typical equity for startup? How should I think about market data for startup equity?

Data sets on employee and executive offer percentages for early stage startups can be misleading and encourage companies to make unrealistically low offers to early hires. There’s two reasons for this. First, these data sets are for employees who are earning something like market level salaries along with equity. Second, these data sets exclude anyone classified as a “founder” from the data set for employees. They keep different data sets for founders! So the gray area between the two classifications makes the use of data tricky. Who is a founder for purposes of the data set? Depends on the data set. Carta, for instance, excludes anyone with 5% or more from the employee/executive data set and classifies them as founders! Even if they are earning market-level cash from their start date.

Here’s the bottom line:

If you are joining before you are being paid startup-phase-market-level cash salary, you are a late stage founder. You should evaluate your equity percentage relative to the other founders within the company or within the market data set.

If you are joining for a combination of cash and equity at an early stage startup, the offer should make sense to you. Simply pointing to market data for the right % ownership is not enough. You’ll want to consider the market data for % ownership in conjunction with the dollar value of the equity based on how investors have most recently valued the company.

Q: How should early-stage startups calculate my percentage ownership?

You'll be negotiating your equity as a percentage of the company's "Fully Diluted Capital." Fully Diluted Capital = the number of shares issued to founders ("Founder Stock") + the number of shares reserved for employees ("Employee Pool") + the number of shares issued to other investors (“preferred shares”). There may also be warrants outstanding, which should also be included. Your Number of Shares / Fully Diluted Capital = Your Percentage Ownership.

Careful, though, because most startups do not issue preferred stock when they take their seed investment funds from their seed investors. Instead, they issue convertible notes or SAFEs. These convert into shares of preferred stock in the next round of funding. So if you negotiate for 1% of a seed stage startup funded with notes or SAFEs, the fully diluted capital number used as the denominator of that calculation does not include the shares to be issued for those seed funds.

How can you address this? First, make sure you know what’s included. You can ask:

How many shares are outstanding on a fully diluted basis? Does this include the full option pool? Are there any shares yet to be issued for investments in the company, such as on SAFEs or convertible notes? How many shares do you expect to issue upon their conversion?

If you are comparing your offer to other seed stage offers or to market data for seed stage offers, you would want to take that into consideration. The number the company provides is only an estimate, of course, but it’s a way to address this in your evaluation.

“Fully Diluted Capital” includes only issued shares and reserved shares. For an early stage startup, that would include founders shares, the option pool, and any preferred shares issued to investors in a priced round. It will not include shares to be issued upon conversion of SAFEs and convertible notes. Therefore, you will want to include some estimate for the conversion of those investments when you are understanding the percentage ownership in an early stage startup offer.

Q: Is there anything tricky I should look out for in my startup equity documents?

Yes. Look for repurchase rights for vested shares.

If so, you may forfeit your vested shares if you leave the company for any reason prior to an acquisition or IPO. In other words, you have infinite vesting as you don't really own the shares even after they vest. This can be called "vested share repurchase rights," "clawbacks” or "non-competition restrictions on equity.”

Most employees who will be subject to this don't know about it until they are leaving the company (either willingly or after being fired) or waiting to get paid out in a merger that is never going to pay them out. That means they have been working to earn equity that does not have the value they think it does while they could have been working somewhere else for real equity.

According to equity expert Bruce Brumberg, "You must read your whole grant agreement and understand all of its terms, even if you have little ability to negotiate changes. In addition, do not ignore new grant agreements on the assumption that these are always going to be the same." When you are exchanging some form of cash compensation or making some other investment such as time for the equity, it makes sense to have an attorney review the documents before committing to the investment.

Q: What is fair for vesting of startup equity?

The standard vesting is monthly vesting over four years with a one year cliff. This means that you earn 1/4 of the shares after one year and 1/48 of the shares every month thereafter. But vesting should make sense. If your role at the company is not expected to extend for four years, consider negotiating for a vesting schedule that matches that expectation.

Q: Should I agree to milestone or performance metrics for my vesting schedule for startup equity?

No. This is a double risk. Not only is there a high risk that the company will not be successful (and the equity worthless), there is a high risk that the milestones will not be met. This is very often outside the control of the employee or even the founders. More on this issue here. The standard is four-year vesting with a one-year cliff. Anything else is off-market and is a sign that the founders are trying to be too creative and reinvent the wheel.

Q: Should I have protection for my unvested shares of startup equity in the event of an acquisition?

Yes. When you negotiate for an equity package in anticipation of a valuable exit, you would hope that you would have the opportunity to earn the full number of shares in the offer so long as you are willing to stay through the vesting schedule.

If you do not have protection for your unvested shares in the stock documents, unvested shares may be cancelled at the time of an acquisition. I call this a “Cancellation Plan.”

Executives and key hires negotiate for “double trigger acceleration upon change of control.” This protects the right to earn the full block of shares, as the shares would immediately become vested if both of the following are met: (1st trigger) an acquisition occurs before the award is fully vested; and (2nd trigger) the employee is terminated after closing before they are fully vested.

There’s plenty of variation in the fine print of double trigger clauses, though. Learn more here.

Q: The company says they will decide the exercise price of my stock options. Can I negotiate that?

A well-advised company will set the exercise price at the fair market value ("FMV") on the date the board grants the options to you. This price is not negotiable, but to protect your interests you want to be sure that they grant you the options ASAP.

Let the company know that this is important to you and follow up on it after you start. If they delay granting you the options until after a financing or other important event, the FMV and the exercise price will go up. This would reduce the value of your stock options.

Early-stage startups very commonly delay making grants. They shrug this off as due to "bandwidth" or other nonsense. But it is really just carelessness about giving their employees what they have been promised.

The timing and, therefore, price of grants does not matter much if the company is a failure. But if the company has great success within its first years, it is a huge problem for individual employees. I have seen individuals stuck with exercise prices in the hundreds of thousands of dollars when they were promised exercise prices in the hundreds of dollars.

Q: What salary can I negotiate as an early-stage employee?

When you join an early-stage startup, you may have to accept a below market salary. But a startup is not a non-profit. You should be up to market salary as soon as the company raises real money. And you should be rewarded for any loss of salary (and the risk that you will be earning $0 salary in a few months if the company does not raise money) in a significant equity award when you join the company.

When you join the company, you may want to come to agreement on your market rate and agree that you will receive a raise to that amount at the time of the financing.

I sometimes see people ask at hire to receive a bonus at the time of the financing to make up for working at below-market rates in the early stages. This is a gamble, of course, because only a small percent of seed-stage startups would ever make it to Series A and be able to pay that bonus. Therefore, it makes far more sense to negotiate for a substantial equity offer instead.

Q: What form of startup equity should I receive? What are the tax consequences of the form?

[Please do not rely on these as tax advice to your particular situation, as they are based on many, many assumptions about an individual's tax situation and the company's compliance with the law. For example, if the company incorrectly designs the structure or the details of your grants, you can be faced with penalty taxes of up to 70%. Or if there are price fluctuations in the year of sale, your tax treatment may be different. Or if the company makes certain choices at acquisition, your tax treatment may be different. Or ... you get the idea that this is complicated.]

These are the most tax advantaged forms of equity compensation for an early-stage employee in order of best to worst:

1. [Tie] Restricted Stock. You buy the shares for their fair market value at the date of grant and file an 83(b) election with the IRS within 30 days. Since you own the shares, your capital gains holding period begins immediately. You avoid being taxed when you receive the stock and avoid ordinary income tax rates at sale of stock. But you take the risk that the stock will become worthless or will be worth less than the price you paid to buy it.

1. [Tie] Non-Qualified Stock Options (Immediately Early Exercised). You early exercise the stock options immediately and file an 83(b) election with the IRS within 30 days. There is no spread between the fair market value of the stock and the exercise price of the options, so you avoid any taxes (even AMT) at exercise. You immediately own the shares (subject to vesting), so you avoid ordinary income tax rates at sale of stock and your capital gains holding period begins immediately. But you take the investment risk that the stock will become worthless or will be worth less than the price you paid to exercise it.

3. Incentive Stock Options ("ISOs"): You will not be taxed when the options are granted, and you will not have ordinary income when you exercise your options. However, you may have to pay Alternative Minimum Tax ("AMT") when you exercise your options on the spread between the fair market value ("FMV") on the date of exercise and the exercise price. You will also get capital gains treatment when you sell the stock so long as you sell your stock at least (1) one year after exercise AND (2) two years after the ISOs are granted.

Q: Who will guide me if I have more questions on startup equity?

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

VIDEO Startup Stock Options: Negotiate the Right Startup Stock Option Offer

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Startup Stock Options - Post Termination Exercise Period - A $1 Million Problem

Negotiating a startup stock option offer? An option exercise extension can save you from a $1M problem. Photo by Pixabay.

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Originally published March 28, 2017. Updated March 17, 2023.

Early Expiration for Startup Stock Options

The startup scene is debating this question: Should employees have a full 10 years from the date of grant to exercise vested options or should their rights to exercise expire early if they leave the company before an IPO or acquisition? This is called a post-termination exercise period or PTEP.

This is Part 1 of a 3-part series. See Early Expiration of Startup Stock Options - Part 2 - The Full 10-Year Term Solution and Early Expiration of Startup Stock Options - Part 3 - Examples of Good Startup Equity Design by Company Stage. See also The Menu of Stock Option Exercise Strategies for more on option exercise planning and startup offer negotiation.

The standard in the past has been that startup stock options are designed with an early expiration period. They must be exercised by whichever comes first:

10 years after the date of grant or

3 months after the last date of employment. (We’ll call this an “early expiration period.")

If a stock option is not exercised by this deadline, it expires and the individual forfeits all rights to the equity they earned. In some cases, this period is shorter, such as expiration 1 month after or even the day of last employment.

If an employee leaves a startup - by choice or involuntary termination of employment - and has to exercise stock options within an early expiration period, he or she has the following choice:

Pay the exercise price and tax bill with savings or a loan;

Find liquidity for some of the shares on the secondary market (which is complicated, not widely accessible, and sometimes prohibited by company or law) to pay for the cost of the exercise price and tax bill; or

Walk away and lose the vested value.

Startup Stock Options’ $1M Problem

This can be a $1 million problem for employees at successful companies because the tax bill due at exercise is based on the value of the shares at exercise. Either ordinary income or alternative minimum taxable (AMT) income may be recognized at exercise. This income will equal the difference between the option exercise price and the value of the shares at the time of exercise. The value of the shares is usually called fair market value (FMV) or 409A valuation. These values are generally set by an outside firm hired by the company. The company may try to set these valuations as low as possible to minimize this problem for employees, but IRS rules generally require that the FMV increases with investor valuations and business successes.

The more successful the company has been between option grant and option exercise, the higher the tax bill will be. For a wildly successful company, the calculation might look like this:

Here’s an example:

Exercise Price = $50,000

FMV at Exercise = $4 million

Gain (either Ordinary Income or AMT Income) Recognized at Exercise = $3,950,000

Hypothetical tax rate = 25%

Taxes Due for Exercise = $1,027,000

Total Exercise Price + Tax Cost to Exercise = $1,077,000

REMEMBER: FMV at exercise is not cash in hand without a liquidity event. Therefore, if the option holder in this example makes the investment of $50,000 plus the tax payment of $1,027,000, they might never realize the $4 million in stock option value they earned, or even reclaim the $1,077,000 exercise price + tax. The shares may never become liquid and could be a total loss. For someone who goes into debt to exercise and pay taxes, that might mean bankruptcy. So, even if they can come up with $1 million to solve the early expiration problem at exercise, they may have wished they had not if the company value later declines.

Investor-types frame this as a simple investment choice - the option holder needs to decide whether or not to bet on the company by the deadline. But many people simply do not have access to funds to cover these amounts. It’s not a realistic choice. The very success of the company they helped create makes it impossible to exercise the stock options they earned.

Although these numbers may seem impossibly large, I regularly see this problem at the $1 million + magnitude for individual option holders. The common demographic for the problem is very early hires of startups that grew to billion-dollar valuations.

Why Now? Later IPOs, Higher Valuations, More Transfer Restrictions

Early expiration of stock options is a hot issue right now because successful startups are staying private longer and staying private after unprecedented valuations. These successful but still private companies have also been enforcing extreme transfer restrictions. These longer timelines from founding to IPO, higher valuations between founding and IPO, and transfer restrictions are causing the early expiration of stock options to affect more employees.

1. Later IPOs = more likely early expiration applies before liquidity. The typical tenure of a startup employee is 3-4 years. As companies stay private longer, employees are more likely to leave a company after their shares have vested but before an IPO. If they have to exercise within the early expiration period but before an IPO, they must pay taxes before they have liquidity to pay the taxes.

2. Higher valuations = higher grant prices. Exercise prices for stock option grants must be set at the fair market value (“FMV” or “409A Value”) of common stock on the date of grant. If an individual joins a company that has had some success in raising funds and in business, the FMV at grant will be higher. Therefore, departing employees are more likely to have hefty exercise prices to pay within an early expiration period. With delayed IPOs they are unlikely to have access to liquidity opportunities to cover exercise prices.

3. Higher valuations = higher tax due at exercise. Total tax bills at exercise are more likely to be high as the company valuations are high because taxable income (either ordinary income or alternative minimum taxable income) is generally equal to FMV at Exercise - Exercise Price. With delayed IPOs, employees are unlikely to have access to liquidity opportunities to cover tax bills.

4. Extreme transfer restrictions = no liquidity prior to IPO or acquisition. In the past, private company stock could be transferred to any accredited investor so long as the seller first offered to sell the shares to the company. (This is known as a right of first refusal or ROFR. The market for pre-IPO stock is known as the secondary market.) Some companies are prohibiting such secondary market transfers and similar structures such as forward sales or loans that had historically allowed employees of hot companies to get liquidity for the shares to pay for exercise costs and tax bills at exercise. Some companies add these transfer restrictions after issuing the shares and even push the limits of the law by claiming that they can enforce new restrictions retroactively.

I hope this post has illuminated the problem of an early expiration period for startup stock options. For more on a solution to the problem, see Early Expiration of Startup Stock Options - Part 2 - The Full 10-Year Term Solution. See also Early Expiration of Startup Stock Options - Part 3 - Examples of Good Startup Equity Design by Company Stage.

Thank You!

Thank you to JD McCullough for providing research assistance for this post. He is a health tech entrepreneur, interested in connecting and improving businesses, products, and people.

Thank you to attorney Augie Rakow, a former partner at Orrick advising startups and investors, for sharing his creative solution to this problem in Early Expiration of Startup Stock Options - Part 2 - The Full 10-Year Term Solution.

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

VIDEO Startup Stock Options: Exercise Price Basics

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Negotiating Equity @ a Startup – Stock Option Counsel Tips

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Negotiating an offer from a startup? Here's some tips.

1. Know How Much Equity You Want

For employees early in their careers, the only negotiable terms for equity are the number of shares of stock and, possibly, the vesting schedule. The company will already have defined the form in which you will earn those shares, such as stock options, restricted stock units or restricted stock.

Your task in negotiating equity is to know how many shares would make the offer appealing to you or better than your other offers. If you don’t know what you want for equity, the company will be happy to tell you that you don’t want much.

Your desired number of shares should be the result of thoughtful consideration of the equity offer. There is no simple way to evaluate equity, but understanding the concepts and playing with the numbers should give you the power to decide how many shares you want.

One way to compare offers and evaluate equity is to find the current VC valuation of the preferred shares in the company. If a VC has recently paid $10 per share for the company’s stock, and you have been offered 10,000 shares, you can use $100,000 to compare to other offers. If another company has offered you 20,000 shares, and a VC has recently paid $5 for their shares, you could use those numbers to compare the offers. For more info on finding VC valuations, see: Startup Valuation Basics or contact Stock Option Counsel.

Remember that the purpose of this exercise is not to have a precise dollar value for the offer, but to answer these questions: How does this offer compare to other offers or my current position? What salary and number of shares at this company would make this a stable, sustainable relationship for me? In other words, will this keep me happy here for some time? If not, it is in nobody’s best interest to come to a deal on that package.

For more information on negotiating equity, see our video: Negotiate the Right Stock Option Offer or our blog with Boris Epstein of BINC Search: Negotiate the Right Job Offer.

2. Look for Tricky Legal Terms That Limit Your Shares' Value

There are some key legal terms that can diminish the value of your equity grant. Pay careful attention to these, as some are harsh enough that it makes sense to walk away from an equity offer.

If you receive your specific equity grant documents before you are hired, such as the Equity Incentive Plan or Stock Option Plan, you can ask an attorney to read them.

If you don’t have the documents, you will have to wait until after you are hired to study the terms. But you can ask some general questions during the negotiation to flush out the tricky terms. For example, will the company have any repurchase rights or forfeiture rights for vested shares? Does the equity plan limit the kinds of exit events in which I can participate? What happens to my equity if I leave the company?

3. Evaluate the Equity’s Potential

Evaluate the company to know how many shares would make the equity offer worth your time. You can start by asking the company some basic questions on their expectations for future growth and the exit timeline.

The higher your rank in the company and the stronger your emphasis on these matters, the more likely you are to speak to the CEO, CFO or someone else at the company who can answer these questions. If you want more resources to help you think like a startup investor, there are great online resources on valuation, dilution and exits for startups.

But don’t place too much weight on the company’s predictions of the equity’s potential value, especially if those values are based on an early-stage company’s Discounted Cash Flows (DCF). Even the experts know that the only thing early stage startups know about financial projections is that they are wrong.

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Best of Blogs: How to Value and Negotiate Startup Stock Options

NOTE: Updated February 23, 2016.

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

We have suggested the following free resources to Stock Option Counsel clients to help them master this area and gain confidence in negotiating their stock options and other employee stock.

1. Leo Polovet's' Analyzing AngelList Job Postings, Part 1: Basic Stats & Part 2: Salary and Equity Benchmarks

2. Venture Hacks' I have a job offer at a startup, am I getting a good deal?

3. Andy Payne's Startup Equity for Employees

4. Mary Russell's Startup Equity Standards: A Guide for Employees

5. Wealthfront's Startup Salary and Equity Compensation Calculator (This is very general but people find it helpful.) And Wealthfront's The Right Way to Grant Equity to Your Employees.

6. Patrick McKenzie of Kalzumeus Software's Salary Negotiation: Make More Money, Be More Valued

7. Piaw Na's Negotiating Compensation, from An Engineer's Guide to Silicon Valley Startups

8. mystockoptions.com's How does a private company decide on the size of a stock grant? (You may have to create a login)

9. Michelle Wetzler's How I Negotiated My Startup Compensation

10. Mary Russell's Video Negotiate the Right Startup Stock Option Offer, based on Mary Russell and Boris Epstein's Bull's Eye: Negotiate the Right Job Offer

11. Mary Russell's Joining An Early Stage Startup? Negotiate Your Salary and Equity with Stock Option Counsel Tips

12. Robby Grossman's Negotiating Your Startup Job Offer

13. John Greathouse's What The Heck Are My Startup Stock Options Worth?! Seven Questions You Should Ask Before Joining A Startup

14. David Weekly's An Introduction to Stock & Options for the Tech Entrepreneur or Startup Employee

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Negotiation Rhythms #2: Best Alternative to Negotiated Agreement

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

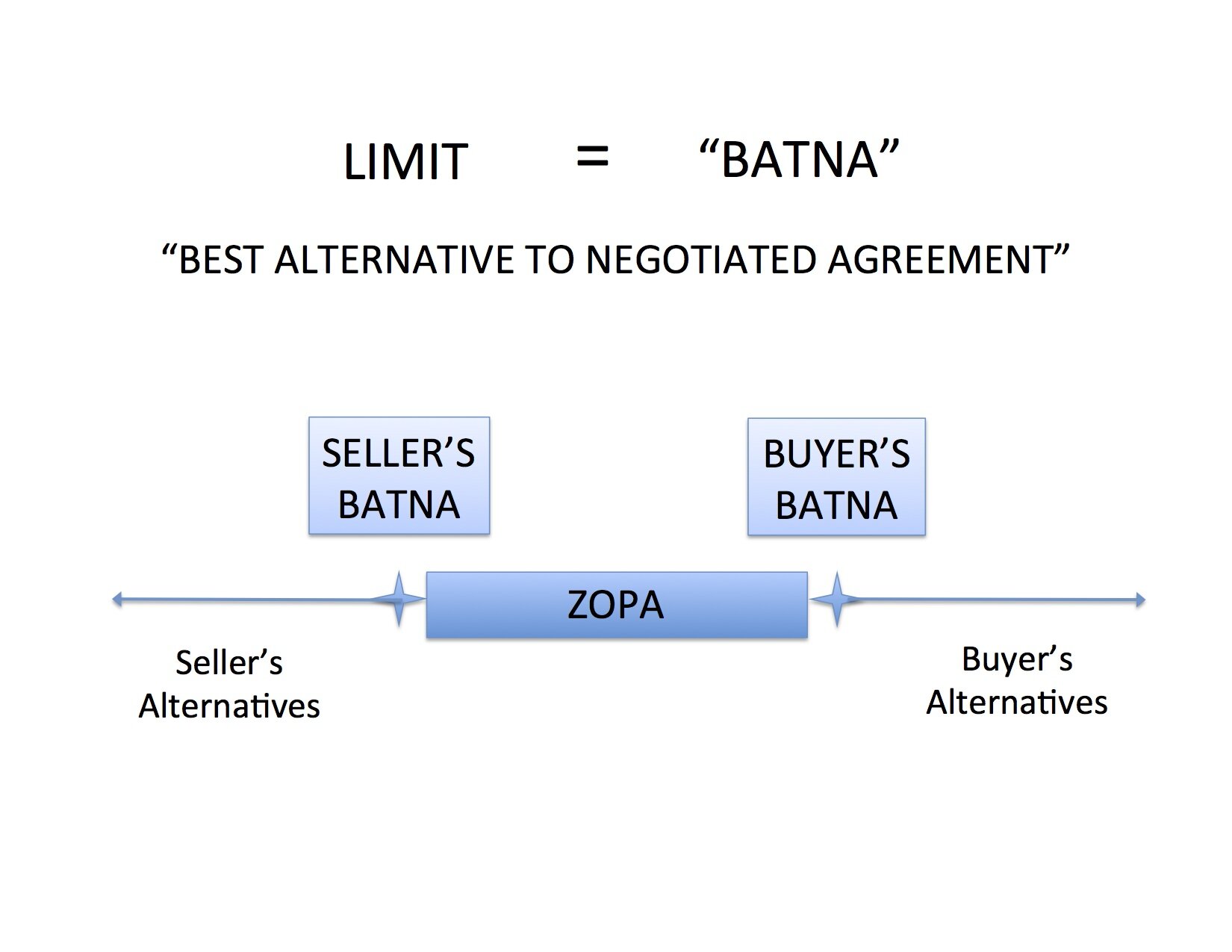

We know we want to push beyond our limits to capture as much value as possible in a negotiation. But how do we define those limits? It takes a five-word phrase to bring this concept into focus: Best Alternative to Negotiated Agreement (“BATNA”).

The BATNA for a car buyer might be the same car at a nearby dealership for $20,000. The BATNA for a home seller might be an offer from another party for $1 million. The BATNA for a child trading baseball cards might be to hold onto his favorite cards and enjoy looking at them rather than to trade them away.

Salary Negotiation Method - Identify your BATNA, or best alternative to negotiated agreement, to find out if there is a ZOPA, or zone of possible agreement.

Any agreement below (or, for a maximum limit, above) a BATNA would leave the negotiator worse off than in the absence of that particular agreement. Said another way, the negotiator would be better off with some other option – their BATNA – than accepting an agreement on those terms.

Salary Negotiation Method - Identify your BATNA, or best alternative to negotiated agreement, to find out if there is a ZOPA, or zone of possible agreement.

To properly identify a BATNA, we must do a lot of calculating, daydreaming, and going out in the world to test alternatives. But this creative process is necessary. When we believe that the only alternative is the one at hand, our negotiation position is dangerously weak. It is also dangerously ineffective because it leads to an arrangement that does not, in fact, make the negotiator better off than without it. And any deal that is not in both parties’ best interests is unstable and likely to collapse after it is made.

Countless factors go into naming and ranking one’s alternatives to arrive at a BATNA, and even then it is impossible to do so clearly as those factors cannot all be outlined in numerical format. A better offer might be less certain of being completed, so it might be more advantageous to make an agreement on less favorable terms today. For example, the other job offer might not be certain even though it appears it would be more advantageous if it were finalized. This is the old saying that a bird in the hand is better than two in the bush, and this can be dangerous for those who optimistically negotiate as if their imaginary alternatives are already in the hand. In the other extreme, this is very limiting for those who are very fearful of uncertainty, as they will accept disadvantageous terms for the simple purpose of having certain terms when a bit of risk in pursuit of a better alternative could have led to greater results.

Timing is important in other ways as well, as a negotiator with more time to come to an agreement will have more chances to find alternatives to the agreement at hand. "Wait and see" becomes a BATNA in itself. The opposite of this would be a party who must have resolution today, which would, of course, limit the alternatives.

Beyond hard limits on time, some people do not enjoy the back and forth process of negotiating. They might prefer to take this deal, and even to accept much less of the middle than is possible to capture, than to continue to seek alternatives or negotiate deals. For these people, the process itself inhibits the growth of BATNAs.

We’ll see in the next post – Negotiation Rhythms #3: Sales & Threats – how brainstorming or eliminating BATNAs changes the ZOPA and improves or weakens our force in negotiation.

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Negotiation Rhythms

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

Salary Negotiation Method: Identify your BATNA, or best alternative to negotiated agreement.

We’ve all heard plenty of advice about negotiating.

The business world directs us to stay rationally focused, rely on exhaustive preparation, think through alternatives, spend less time talking and more time listening and asking questions, and let the other side make the first offer.[1]

The psych world counsels us to listen first, sit down, find common ground, move in, keep cool, be brief, forget neutrality, avoid empty threats, and don’t yield.[2]

These tips don’t have much meaning without knowing the underlying principles of negotiations, and studying tips alone is about as meaningful as learning dance steps without ever hearing the music.

The following three-part series presents the rhythm of negotiations as described in the Harvard Negotiation Project’s Getting to Yes: Negotiating Agreement Without Giving In.[3] It should be useful for those first learning to hear this rhythm and for those who have been dancing since the bazaars of their youth who may need to go back to basics to learn some tricky new steps.

Read on!

#1: Zone of Possible Agreement

#2: Best Alternatives to Negotiated Agreement

#3: Sales & Threats

Attorney Mary Russell counsels individuals on startup equity, including:

You are welcome to contact her at (650) 326-3412 or at info@stockoptioncounsel.com.

[1] Take It Or Leave It: The Only Guide to Negotiating You Will Ever Need http://www.inc.com/magazine/20030801/negotiation.html via @Inc

[2] The Art of Negotiation | Psychology Today http://www.psychologytoday.com/articles/200701/the-art-negotiation

[3] Roger Fisher, William Ury and Bruce Patton, Getting to Yes: Negotiating Agreement Without Giving In.